Why the shilling is under pressure despite strong economic growth

A review of Tanzania’s exchange-rate history suggests that the current movement is neither unprecedented nor disconnected from long-established seasonal cycles that have shaped the performance of the shilling for more than two decades

Dar es Salaam. The Tanzanian shilling has continued to lose ground against the United States dollar during the first half of 2026, extending a pattern that economists and central bank officials describe as largely seasonal rather than a sign of underlying economic distress.

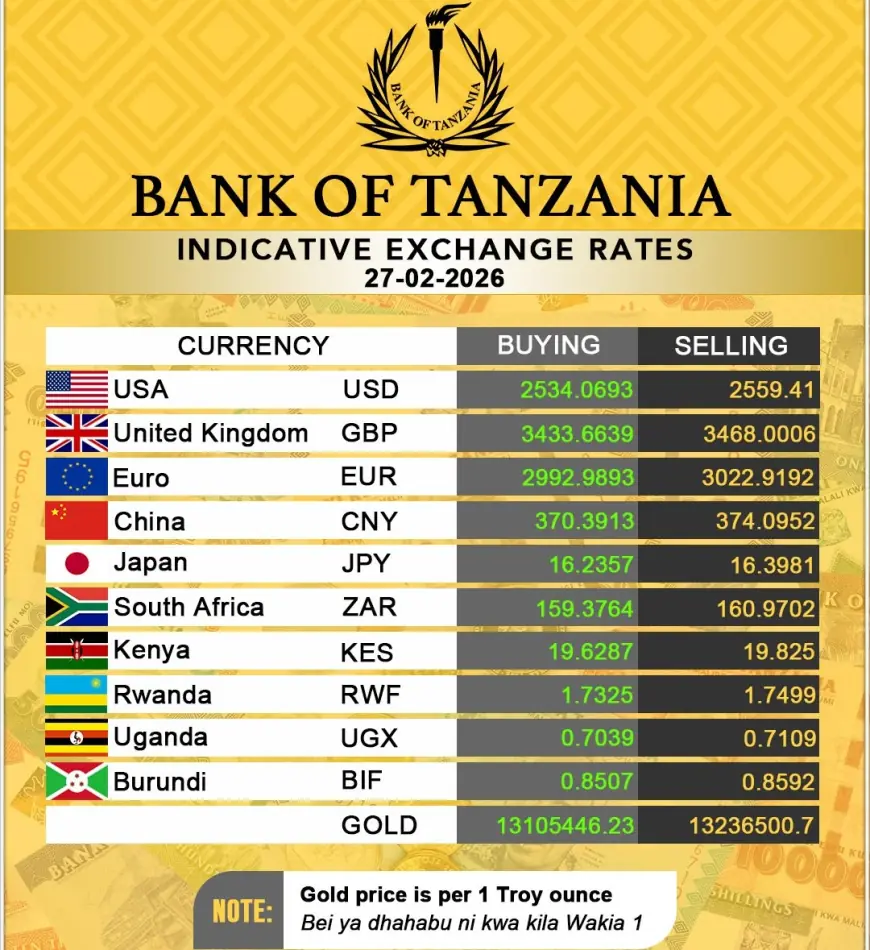

Data published by the Bank of Tanzania (BoT) show a gradual but persistent depreciation of the local currency between February and June, with the indicative selling rate of the dollar moving from about Sh2,559 at the end of February to more than Sh2,644 by June 19.

A review of Tanzania’s exchange-rate history suggests that the current movement is neither unprecedented nor disconnected from long-established seasonal cycles that have shaped the performance of the shilling for more than two decades.

The BoT indicative rates show that on February 27, 2026, the dollar was selling at Sh2,559.41.

By March 31, the rate had risen to Sh2,594.41, indicating a weakening of the shilling.

The depreciation continued through June.

On June 5, the selling rate reached Sh2,619.66 before rising to Sh2,627.00 on June 9.

The dollar was quoted at Sh2,629.63 on June 11, Sh2,635.56 on June 16, Sh2,641.35 on June 17 and Sh2,642.92 on June 18.

By June 19, the indicative selling rate stood at Sh2,644.11.

Historical precedents

Although the movement appears significant over a relatively short period, analysis by Doing Business shows that the shilling has historically experienced similar bouts of weakness during the first half of the year, when foreign exchange inflows from key export sectors typically decline while import demand remains elevated.

Bank of Tanzania Governor Emmanuel Tutuba has repeatedly attributed the current pressures to seasonal market dynamics.

According to the central bank, foreign currency earnings from agriculture, mining and tourism tend to slow between January and May, creating temporary shortages in the market even as businesses continue to require dollars to finance imports.

The situation is often compounded by increased import orders from Asia, particularly around the period preceding the Chinese New Year, when Tanzanian traders seek to secure inventories and industrial inputs.

The resulting surge in demand for dollars places additional pressure on the local currency.

Historical exchange-rate data indicate that the shilling traded at around Sh1,041 per US dollar in late 2004 before gradually weakening during 2005.

By the second half of that year, the exchange rate had moved into the Sh1,130–Sh1,170 range against the dollar, reflecting rising demand for foreign currency and broader shifts in international markets.

Coverage of the currency during 2004, 2005 and the first half of 2006 frequently focused on the balance between export earnings and import requirements.

At the time, economists pointed to strong demand for imported fuel, machinery, industrial equipment and consumer goods as key drivers of dollar demand.

Harvest cycles

Meanwhile, the country's dependence on a relatively narrow export base meant that foreign exchange inflows fluctuated according to harvest cycles and global commodity prices.

Two decades later, many of those structural characteristics remain visible, although Tanzania's economy has become larger, more diversified and considerably more resilient.

Today, gold, tourism, transport services, manufactured exports and a growing range of agricultural products contribute substantially to foreign exchange earnings.

The country has also accumulated stronger foreign exchange reserves and developed more sophisticated monetary policy tools than were available in the mid-2000s.

Nevertheless, economists caution that even a stronger economy does not automatically translate into a stronger currency.

Recent BoT research has underscored that exchange-rate depreciation alone cannot resolve trade imbalances.

The central bank argues that sustainable improvement in the external sector depends on export diversification, higher productivity and expanded manufacturing capacity rather than currency movements alone.

Export peformance

Another central bank study covering data from 1997 to 2023 found that while depreciation can support export performance, its impact is relatively modest and works best when accompanied by broader improvements in production and competitiveness.

The current depreciation is unfolding against a backdrop of generally favourable macroeconomic conditions.

Inflation remains within the government's target range, while economic growth continues to be supported by strong performance in agriculture, mining, construction and services.

The BoT has maintained a relatively accommodative monetary stance, keeping the Central Bank Rate unchanged at 5.75 percent during the first part of the year as inflationary pressures remained contained.

Export earnings from gold and tourism have also provided an important cushion.

Gold remains one of Tanzania's leading sources of foreign exchange, bringing in $5.2 billion in the year ending March 2026.

Tourism continues to generate substantial dollar inflows that help support the balance of payments.

Intervention

The central bank has meanwhile continued to intervene in the interbank foreign exchange market whenever necessary to smooth excessive volatility and ensure orderly market conditions.

For businesses, the weakening shilling presents both opportunities and challenges.

Exporters generally benefit because goods priced in dollars generate higher returns when converted into local currency.

Tourism operators can also gain a competitive advantage as Tanzania becomes relatively cheaper for foreign visitors.

On the other hand, importers face higher costs for fuel, machinery, pharmaceuticals, industrial raw materials and other products purchased abroad.

The principal concern for policymakers is whether a prolonged depreciation could eventually feed into domestic prices through more expensive imports.

So far, inflation has remained relatively subdued, suggesting that the pass-through effect has been limited.

Most economists therefore view the current movement not as a currency crisis but as a reflection of seasonal demand-and-supply dynamics in the foreign exchange market.

They expect conditions to improve as export receipts from agriculture, mining and tourism strengthen during the second half of the year, increasing the supply of foreign currency and easing pressure on the shilling.

For now, the trajectory of the shilling appears to be following a familiar pattern.

Much as it did in 2004, 2005 and the first half of 2006, the currency is responding to the interplay between seasonal foreign exchange inflows and persistent import demand.

The difference today is that the economy underpinning the currency is larger, more diversified and better equipped to absorb temporary shocks, even as the dollar continues to command a premium in the market.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0