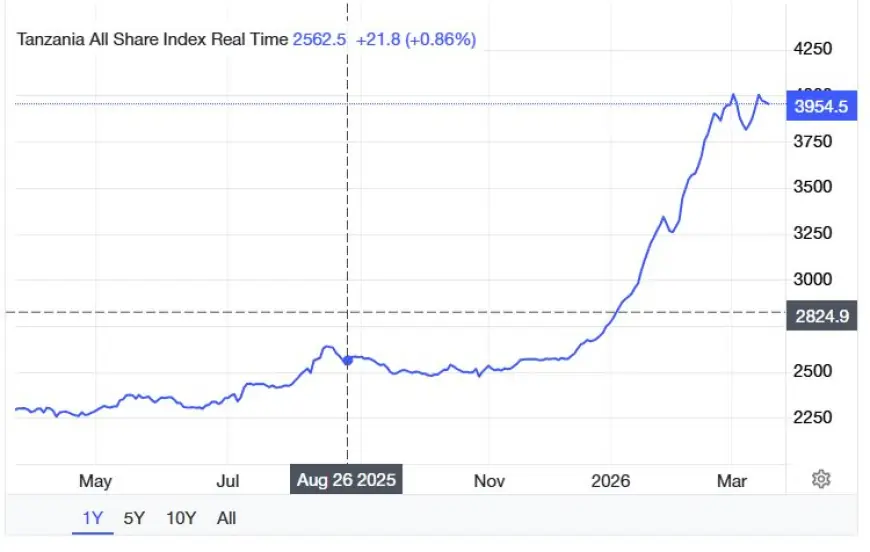

Dar es Salaam Stock Exchange rebounds with extraordinary gains in second week of March 2026

The market was heavily dominated by banking sector activity, particularly CRDB, which traded a remarkable 12.49 million shares over the five-day period

Dar es Salaam. The Dar es Salaam Stock Exchange (DSE) closed second week of March 2026 on a distinctly bullish note, driven by heightened trading activity, substantial gains in select equities, and renewed investor conviction, according to market analysis.

Following a period of market correction in previous sessions, investor sentiment surged between March 9 and 13, leading to massive price appreciations in select counters and a significant expansion in total market capitalisation.

According to analyses by TanzaniaInvest and Tanzania Securities Limited (TSL), the exchange witnessed a bullish run that saw Equity Turnover grow by 42.31 percent, reaching Sh42.68 billion.

This robust performance was mirrored by the Total Market Capitalisation, which expanded by 4.15 percent to close at Sh34.52 trillion, supported largely by a decisive return of risk appetite amongst domestic investors.

It reflected a 4.15 percent increase from the Week 10 close of Sh33.14 trillion.

Conversely, ETF Market Capitalisation recorded a slight decline of 0.41 percent to Sh190.50 billion, halting the rapid growth observed during the previous week.

Equity market performance and volumetric surge

The equities market was characterised by a substantial increase in both value and volume.

CRDB Bank emerged as the primary engine of liquidity, dominating market activity by trading 12.49 million shares.

This massive volume was bolstered by significant pre-arranged block trades throughout the week, particularly on Monday (2.53 million shares), Tuesday (960,000 shares), and Wednesday (1.23 million shares).

DCB Commercial Bank maintained its position as the second-most-traded stock, consistently moving heavy volumes on the normal board to accumulate 1.32 million shares throughout the week.

Other notable mid-week block trades included KCB’s 235,000 shares on Wednesday and TBL’s 100,000 shares on Friday.

While the Exchange Traded Fund (ETF) board saw a decrease in turnover to Sh1.58 billion compared to the previous week's explosive figures (Sh8.37 billion), daily activity remained consistent across the IEACLC-ETF and VERTEX-ETF instruments.

Block trades further supported ETF activity, including 200,000 units of the IEACLC-ETF on Tuesday and 320,000 units on Friday.

Sectoral indices and extraordinary individual gains

The recovery was broad-based, with four out of five DSE benchmarks advancing.

The Commercial Services (CS) Index and the All Share Index (DSEI) also posted gains of 4.23 percent and 4.15 percent respectively.

Individual stock performances were headlined by PAL, which recorded a staggering appreciation of 156.06 percent, skyrocketing from Sh330 to close the week at Sh845.

TTP followed with a surge of 52.17 percent to close at Sh700.

Conversely, the Industrial Allied (IA) Index was the sole decliner, slipping by a marginal 0.34 percent, while MKCB and MBP faced selling pressure, dropping 6.37 percent and 5.59 percent respectively.

Fixed income and investor demographics

The debt market remained a pillar of stability and liquidity, with bond turnover rising to Sh172.64 billion.

The 20-year Treasury bonds alone accounted for approximately 32 percent of the overall market turnover, underscoring a clear investor preference for longer-dated securities in the current economic climate.

Corporate bond activity remained minimal, with only a single transaction involving a 5-year bond recorded on Tuesday.

Local investors drove 100 percent of the total purchases, valued at Sh42.67 billion, signaling a powerful domestic conviction in the Tanzanian market.

However, this was countered by foreign investors who dominated the sell side, contributing 69.4 percent of total disposals.

The resilience of the DSE during Week 11 suggests that the market has successfully absorbed the earlier corrections of 2026.

With institutional focus remaining sharp on financial and consumer blue-chips, analysts anticipate that the current momentum may provide a stable foundation for the remainder of the quarter.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0